How are interest swaps settled?

How are interest swaps settled?

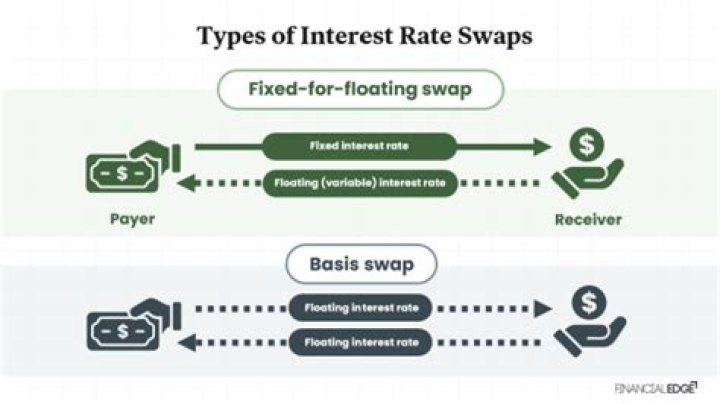

In this swap, Party A agrees to pay Party B a predetermined, fixed rate of interest on a notional principal on specific dates for a specified period of time. The specified payment dates are called settlement dates, and the times between are called settlement periods.

What is the settlement date on interest rate swap?

Settlement Date: The settlement date is the agreed date that the counterparties will exchange the cash flows (interest rate payments). Settlement Period: The settlement period is the length of time between two settlement dates. The settlement periods depend on the agreement of the counterparties.

How is swap value calculated?

Interest rate swap value is determined by summing up the present values of its cash flows, starting with determining the correct discount factor (df), calculated for each period (t) of the cash flow.

How is fixed swap rate calculated?

It means that the fixed rate on the swap (let’s call it c) equals 1 minus the present value factor that applies to the last cash flow date of the swap divided by the sum of all the present value factors corresponding to all the swap dates.

How is settlement date calculated?

The settlement date for stocks and bonds is usually two business days after the execution date (T+2). For government securities and options, it’s the next business day (T+1). In spot foreign exchange (FX), the date is two business days after the transaction date.

How do you calculate expected settlement date?

For most stock trades, settlement occurs two business days after the day the order executes, or T+2 (trade date plus two days). For example, if you were to execute an order on Monday, it would typically settle on Wednesday.

How do you value an interest rate swap?

Therefore, such swap contracts can be valued in terms of fixed-rate and floating-rate bonds. Let’s denote the annual fixed rate of the swap by c, the annual fixed amount by C, and the notional amount by N. Thus, the investment bank should pay c/4*N or C/4 each quarter and will receive the LIBOR rate multiplied by N.

What happens on settlement date?

On settlement day, at an agreed time and place, your settlement agent (solicitor or conveyancer) meets with your lender and the seller’s representatives to exchange documents. They organise for the balance of the purchase price to be paid to the seller.

What is t3 settlement date?

T+3. The settlement date for securities transactions such as a stock sale. It refers to the obligation in the brokerage business to settle securities trades by the third day following the trade date.

What is the difference between value date and settlement date?

The value date is the day that the currencies are traded, not the date on which the traders agree to the exchange rate. The trade date is the date on which a transaction was executed. The settlement date is the date on which a transaction is completed. The value date is usually, but not always, the settlement date.