How do you consolidate accounts of subsidiaries?

How do you consolidate accounts of subsidiaries?

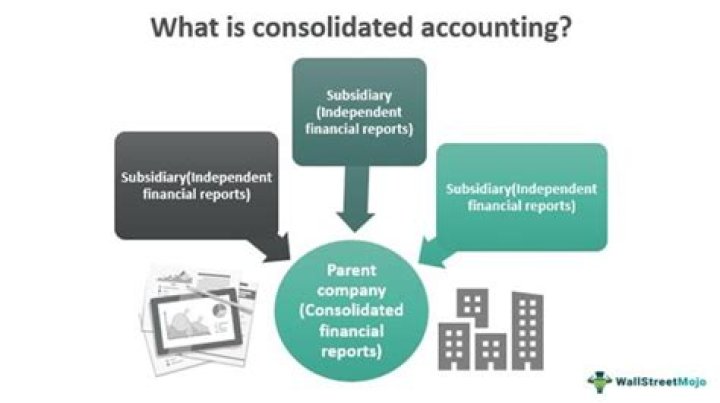

The consolidation method works by reporting the subsidiary’s balances in a combined statement along with the parent company’s balances, hence “consolidated”. Under the consolidation method, a parent company combines its own revenue with 100% of the revenue of the subsidiary.

How should a subsidiary be accounted for in the consolidated financial statements?

If a company has ownership in subsidiaries but does not choose to include a subsidiary in complex consolidated financial statement reporting then it will usually account for the subsidiary ownership using the cost method or the equity method.

Which are examples consolidation?

The definition of consolidation means the act of combining or merging people or things. An example of a consolidation is when two companies merge together. A consolidating or being consolidated. A merger; union.

What are consolidated subsidiaries?

Consolidated Subsidiaries means each Subsidiary of the Borrower (whether now existing or hereafter created or acquired) the financial statements of which shall be (or should have been) consolidated with the financial statements of the Borrower in accordance with GAAP.

When should you consolidate accounts?

Consolidated financial statements are used when the parent company holds a majority stake by controlling more than 50% of the subsidiary business. Parent companies that hold more than 20% qualify to use consolidated accounting. If a parent company holds less than a 20% stake, it must use equity method accounting.

What are the methods of consolidation?

There are three consolidation methods, which are used depending on the strength of the Parent company’s control or influence (see also Significant influence): Full consolidation, Proportionate consolidation, and the Equity method.

How is a consolidated balance sheet prepared explain?

A consolidated balance sheet is usually prepared by the business operating as a group of companies that have more than one subsidiary and it portrays the combined details of assets and liabilities.

Who should prepare consolidated financial statements?

Who will prepare the Consociated Financial Statement? As stated in Section 129 It is duty of the Parent Company (Management) to prepare the consolidated financial statement of the company and laid the same before the Annual General Meeting along with Stand alone financial statement.

What do you mean by consolidation give an example with steps?

Data consolidation is the corralling, combining, and storing of varied data in a single place. Step 1: Open all files (workbooks) that contain the data you want to consolidate. Step 2: Ensure the data is organized in the same way (see example below). Step 3: On the Data ribbons, select Data Tools and then Consolidate.

What is included in consolidated financial statements?

Consolidated financial statements are financial statements that present the assets, liabilities, equity, income, expenses and cash flows of a parent and its subsidiaries as those of a single economic entity.

What is the purpose of consolidated financial statements?

The purpose of consolidated financial statements is to present, primarily for the benefit of the owners and creditors of the parent, the results of operations and the financial position of a parent and all its subsidiaries as if the consolidated group were a single economic entity.