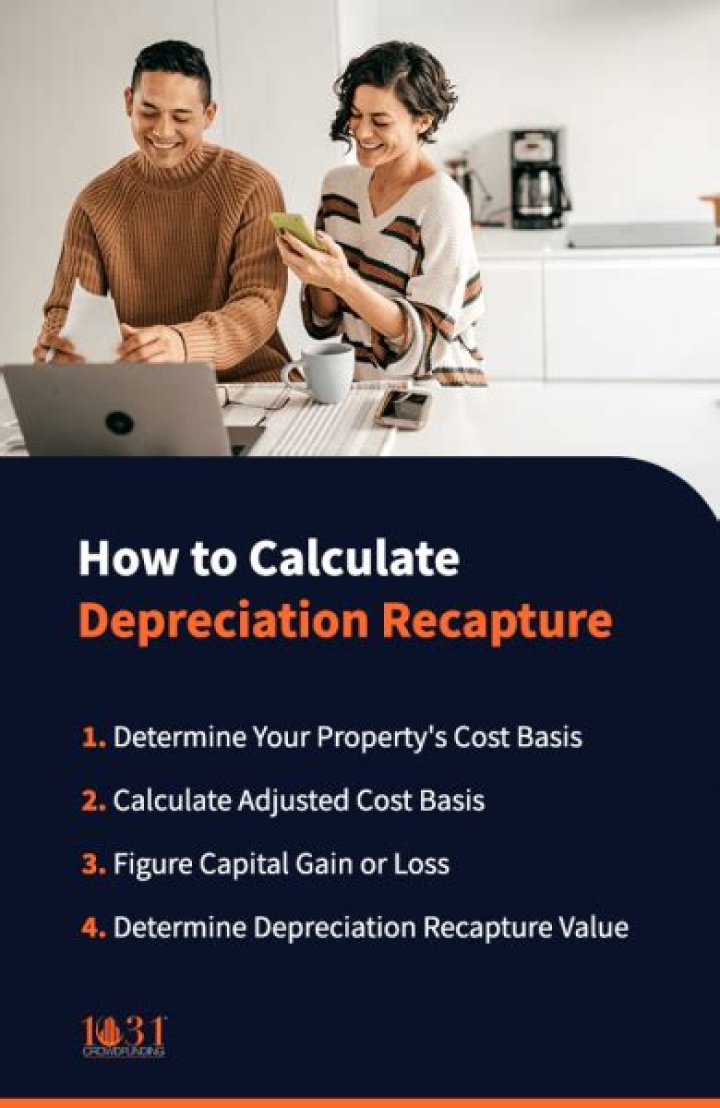

How do you recapture depreciation

Depreciation recapture is assessed when the sale price of an asset exceeds the tax basis or adjusted cost basis. The difference between these figures is thus “recaptured” by reporting it as ordinary income. Depreciation recapture is reported on Internal Revenue Service

How do you calculate depreciation recapture?

Subtract the taken or allowable depreciation expense from your original cost basis. This amount is your adjusted cost basis. For example, if you paid $10,000 for a tractor and took $4,000 in depreciation expenses, your new adjusted cost basis would be $10,000 minus $4,000, or $6,000.

How do you calculate recapture?

Start with your UCC in any class and add the amount you spent on new property in the class. Then, subtract the proceeds you earned from the disposition of property in that class.

How do you avoid paying depreciation recapture?

Investors may avoid paying tax on depreciation recapture by turning a rental property into a primary residence or conducting a 1031 tax deferred exchange. When an investor passes away and rental property is inherited, the property basis is stepped-up and the heirs pay no tax on depreciation recapture or capital gains.How do you calculate depreciation recapture on equipment?

You could then determine the asset’s depreciation recapture value by subtracting the adjusted cost basis from the asset’s sale price. If you bought equipment for $30,000 and the IRS assigned you a 15% deduction rate with a deduction period of four years, your cost basis is $30,000.

What happens to depreciation when you sell?

Depreciation will play a role in the amount of taxes you’ll owe when you sell. Because depreciation expenses lower your cost basis in the property, they ultimately determine your gain or loss when you sell. … If you hold the property for at least a year and sell it for a profit, you’ll pay long-term capital gains taxes.

When you sell a rental property do you have to pay back depreciation?

If you decide to sell your rental property for more than its current depreciated value, you will be required to pay what is referred to as the depreciation recapture tax. Essentially, this amounts to a 25 percent tax on the amount above depreciation value that your property sells for.

Does 1031 avoid depreciation recapture?

1031 Exchanges allow you to defer both the capital gains tax and depreciation recapture from the sale of a property and invest the proceeds into another “like-kind” property, often called “trading up.”What happens to unused depreciation when you sell a rental property?

The short answer is no. Unused depreciation doesn’t become a deduction when you sell a rental property. But like most real estate tax topics, there’s quite a bit more to the story.

What happens when rental property is fully depreciated?It depends but in this instance, the residential rental property will be considered fully depreciated after 27.5 year. … According to the IRS, You must stop depreciating property when the total of your yearly depreciation deductions equals your cost or other basis of your property.

Article first time published onDo I take depreciation in the year of sale?

First, to establish account balances that are appropriate at the date of sale, depreciation is recorded for the period of use during the current year. … Second, the amount received from the sale is recorded while the book value of the asset (both its cost and accumulated depreciation) is removed.

How do I report depreciation recapture on my tax return?

The recapture amount is included on line 31 (and line 13) of Form 4797. See the instructions for Part III. If the total gain for the depreciable property is more than the recapture amount, the excess is reported on Form 8949.

How do you calculate depreciation recapture on rental property?

- Total recognized gain = $176,360.

- Depreciation expense = $36,360 x 24% ordinary tax rate = $8,726 tax based on income bracket.

- Remaining gain = $176,360 – $36,360 depreciation expense = $140,000 x 15% = $21,000 tax based on capital gains.

Is depreciation recapture always 25 %?

Depreciation recaptures on gains specific to real estate property are capped at a maximum of 25% for 2019. To calculate the amount of depreciation recapture, the adjusted cost basis of the asset must be compared to the sale price of the asset.

How do you calculate 1250 recapture?

Section 1250 recapture is calculated as the lesser of: (1) the excess of accelerated depreciation claimed on real property over what would have been allowed under the straight-line method, or (2) the gain realized upon disposition. There is also a concept known as unrecaptured Section 1250 gain.

How much tax do I owe recapture?

The maximum recapture tax is either 50% of the gain on sale or 6.25% of the original loan amount, whichever is less.

What is the depreciation recapture tax rate for 2021?

Depreciation recapture is the portion of the gain attributable to the depreciation deductions previously allowed during the period the taxpayer owned the property. The depreciation recapture rate on this portion of the gain is 25%.

Where does depreciation recapture go on 1040?

Depreciation allowed is the amount that must be recaptured as ordinary income and is reported on Form 4797, Part II, then carries to Form 1040, Line 14.

How many years can I depreciate my house?

By convention, most U.S. residential rental property is depreciated at a rate of 3.636% each year for 27.5 years. Only the value of buildings can be depreciated; you cannot depreciate land.

How long do I have to live in a rental property to avoid capital gains tax?

If you like your rental property enough to live in it, you could convert it to a primary residence to avoid capital gains tax. There are some rules, however, that the IRS enforces. You have to own the home for at least five years. And you have to live in it for at least two out of five years before you sell it.

What is the capital gain tax for 2020?

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300

Can you sell a fully depreciated asset?

Selling Depreciated Assets When you sell a depreciated asset, any profit relative to the item’s depreciated price is a capital gain. … If you used the Section 179 deduction, for example, to write down the cost of the computer to nothing and sold it for $1,200, the entire selling price would be a taxable gain.

What can I claim when selling investment property?

Repairs and maintenance to your investment property. Management and maintenance costs, including strata fees, council rates, water rates, cleaning, gardening and pest control fees. Insurance for your investment property, including building, landlord and contents insurance. Interest on your mortgage and borrowing …

How much depreciation can you write off?

Section 179 Deduction: This allows you to deduct the entire cost of the asset in the year it’s acquired, up to a maximum of $25,000 beginning in 2015. Depreciation is something that should definitely be appreciated by small business owners.

Do you have to recapture Section 179 depreciation?

When Must You Recapture the Deduction? You may have to recapture the section 179 deduction if, in any year during the property’s recovery period, the percentage of business use drops to 50% or less.

What IRS form do I use to report sale of rental property?

Report the gain or loss on the sale of rental property on Form 4797, Sales of Business Property or on Form 8949, Sales and Other Dispositions of Capital Assets depending on the purpose of the rental activity.

Can rental property depreciation offset ordinary income?

Depreciation is one of the biggest and most important deductions for rental real estate investors because it reduces taxable income but not cash flow. … That’s a huge benefit that can offset the income generated by the rental property—ultimately lowering your year-end tax burden.

Can you stop taking depreciation on rental property?

Rental Property Depreciation The expected useful life of a rental property is 27.5 years, according to the IRS. … After the entire cost basis has been deducted over 27.5 years, depreciation ends. Depreciation can also stop after the property is sold or the rental property has stopped producing income.

How do you calculate capital gains recapture and depreciation?

- 1.) First, calculate the adjusted tax basis: …

- 2.) Calculate the realized gain: …

- 3.) The depreciation recapture value is the amount of depreciation taken multiplied by a 25% rate: …

- 4.) The remaining gain is taxed at the capital gains rate of 0%, 15%, or 20%:

How do you calculate capital gains on sale of rental property?

To calculate the capital gain on the property, subtract the cost basis from the net proceeds. If it’s a negative number, you have a loss. But if it’s a positive number, you have a gain.

What happens to depreciation recapture in a 1031 exchange?

Taxable Sale1031 ExchangeBuying Power (putting 25% down)$17,061,540$20,000,000