Is Job Order Costing a traditional costing system

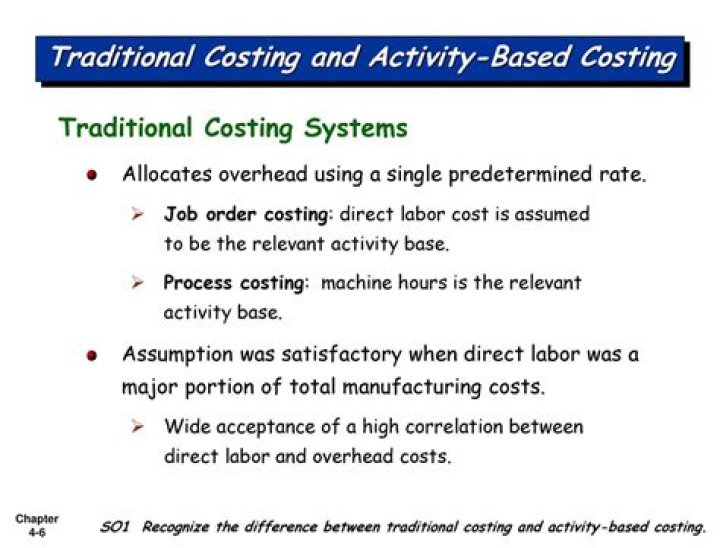

As we saw, there are two traditional costing methods that companies use to assign costs to the products and/or services that they provide: job order costing and process costing. … As we learned, job order costing assigns costs to specific units or products.

What type of costing is job order?

Job order costing is a costing method which is used to determine the cost of manufacturing each product. This costing method is usually adopted when the manufacturer produces a variety of products which are different from one another and needs to calculate the cost for doing an individual job.

Would a job order costing system or a process costing system be used for the production process?

Job costing is used for very small production runs, and process costing is used for large production runs. … Much more record keeping is required for job costing, since time and materials must be charged to specific jobs. Process costing aggregates costs, and so requires less record keeping.

Is job costing a method of costing?

Job costing is a costing method used to determine the cost of specific jobs, which are performed according to the customer’s specifications. It is a basic costing method which is applicable where work consists of separate projects or contract jobs.What is a job order system?

Job order costing is a system that takes place when customers order small, unique batches of products. This system determines the price of each individual product and ensures that the cost for each product is reasonable enough for a customer to purchase it while still allowing the company to make a profit.

What is job order costing mention its feature?

Job costing is a method of cost accounting whereby cost is compiled for a specific quantity of product, equipment, repair or other service that moves through the production process as a continuously identifiable unit, applicable material, direct labour, direct expenses and usually a calculated portion of overheads …

What are the main characteristic of job order costing?

- The products are produced only against customer’s order and not for maintaining stock for sale.

- The costs are accumulated to each job separately.

- A job is performed according to the customer’s specifications.

- The job costing method falls under the category of specific order costing.

What are the primary differences between job costing system and process costing system?

Production: In job costing, production is customized, while it is standardized in process costing. Assignment: In job costing, it is calculating the cost of each job. In process costing, the cost is first determined by the process and then decided based on the number of units produced.How does job order costing system differ from process costing system?

Job order costing tracks prime costs to assign direct material and direct labor to individual products (jobs). Process costing also tracks prime costs to assign direct material and direct labor to each production department (batch).

What is the difference between job order costing and process costing quizlet?Process costing is used when a single product is produced on a continuing basis or for a long period of time. Job-order costing is used when many different jobs having different production requirements are worked on each period.

Article first time published onCan a business use both a job order cost system and a process cost system?

Your business can use job order costing and process costing to track production costs and allocate expenses, such as time, materials and labor, to your products, and both use about the same information to calculate unit cost.

When using a job costing system costs classified as work in process inventory are categorized according to the Associated?

When using a job costing system, costs classified as work-in-process inventory are. categorized according to the associated: Output.

Which is not similarity between job order costing and process costing?

Q.Which is not a similarity between job order costing and process costing?B.Tracking of direct materials, direct labor and manufacturing overheadC.Accumulating journal entriesD.Flow of costsAnswer» a. Methods of assigned costs

How are costs accumulated in a job order costing system?

What is a Job Order Costing System? A job order costing system accumulates the costs associated with a specific batch of products. This system is used for small batch sizes, and especially when the products within each batch are different from the products created in other batches.

How are costs accumulated in job order costing?

Job costing accumulates costs by individual jobs. Process costing accumulates costs by process or department. Work in Process Inventory accounts. Job cost systems have one Work in Process Inventory account for each job.

Who uses a job costing system?

First, companies producing individual, unique products known as jobs use job costing (also called job order costing). Companies such as construction companies and consulting firms, produce jobs and use job costing. Second, some companies, like furniture manufacturers, produce batches of products.

What is job costing describe the difference between job costing and contract costing?

Job costing is the ascertaining of costs that are incurred in the undertaking of a specific job. On the other hand, contract costing is the ascertaining of costs associated with the production of a specific product as per the contract agreement with the customer.

What is job costing What are the main features of job costing How does it differ from batch costing?

The key difference between job costing and batch costing is that job costing is a system used for completion of specific customer orders where each unit produced is considered a job whereas batch costing is a method of costing when a number of identical units are produced in a batch, but each batch is different.

Can a company use both job order costing and process costing Why or why not?

Process costing and job order costing are both acceptable methods for tracking costs and production levels. Some companies use a single method, while some companies use both, which creates a hybrid costing system. The system a company uses depends on the nature of the product the company manufactures.

What type of companies can use job order costing or process costing?

Companies in the white collar sector of business, including law firms, accounting businesses and private investment companies, can utilize job order costing to manage individual client accounts. For example, accounting firms can consider each individual client a job.

Which one of the following is a characteristic that job order cost systems and process cost systems have in common?

Which one of the following is a characteristic that job-order cost systems and process cost systems have in common? Both systems are used for custom made, unique products. The objective is to determine the efficiency of production.

How does ABC differ from traditional absorption costing?

Absorption costing and activity-based costing differ in approach. Absorption costing assigns costs to individual units, whereas activity-based costing focuses on company activities as a central cost and then attempts to assign indirect costs to units.

How is the cost of spoilage losses disposed in a job order costing system?

Accounting for Spoilage in Job Costing. The disposal value of the spoilage is credited to work-in-progress control account and also to the specific job account. The materials control account and spoiled goods disposal value or income account are debited with the disposal value.

What are three major types of manufacturing costs that are accounted for in a job order cost system?

A job order cost accounting system allocates costs to each job. The costs allocated are the three product costs we learned in Chapter 14: materials, direct labor, and factory overhead. The following summarizes the primary source documents used in a factory to allocate these costs.

What are transferred in costs as used in a process costing system?

Transferred-in costs are the costs accumulated by the product at any given point in production. They are “transferred in” to the new business department that receives the partially finished product and is responsible for continuing the production process.