Is R and correlation the same?

Is R and correlation the same?

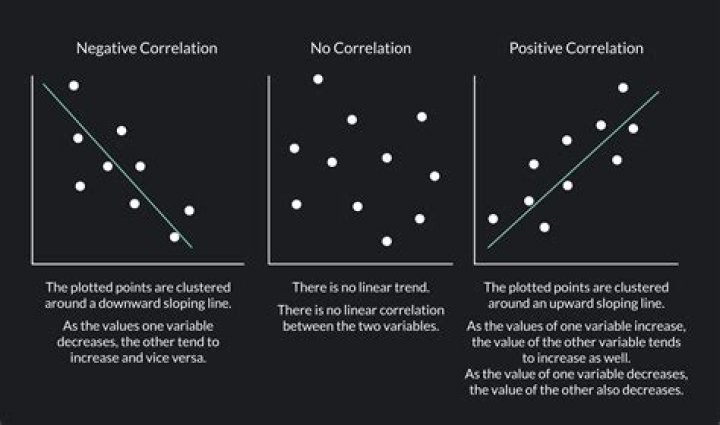

Correlation quantifies the degree to which two variables are related. Correlation does not fit a line through the data points. You simply are computing a correlation coefficient (r) that tells you how much one variable tends to change when the other one does. When r is 0.0, there is no relationship.

Is R-squared the correlation value?

The correlation, denoted by r, measures the amount of linear association between two variables. The R-squared value, denoted by R 2, is the square of the correlation. It measures the proportion of variation in the dependent variable that can be attributed to the independent variable.

Do you use R or R-squared for correlation?

Coefficient of correlation is “R” value which is given in the summary table in the Regression output. R square is also called coefficient of determination. Multiply R times R to get the R square value. In other words Coefficient of Determination is the square of Coefficeint of Correlation.

How do you explain R-squared?

R-squared evaluates the scatter of the data points around the fitted regression line. For the same data set, higher R-squared values represent smaller differences between the observed data and the fitted values. R-squared is the percentage of the dependent variable variation that a linear model explains.

What is R-squared and adjusted R-squared?

R-squared measures the proportion of the variation in your dependent variable (Y) explained by your independent variables (X) for a linear regression model. Adjusted R-squared adjusts the statistic based on the number of independent variables in the model.

What does an R-squared value of 0.8 mean?

80%

R-squared or R2 explains the degree to which your input variables explain the variation of your output / predicted variable. So, if R-square is 0.8, it means 80% of the variation in the output variable is explained by the input variables.

What does R-squared tell you in regression?

R-squared is a goodness-of-fit measure for linear regression models. This statistic indicates the percentage of the variance in the dependent variable that the independent variables explain collectively. After fitting a linear regression model, you need to determine how well the model fits the data.

Should I use R2 or adjusted R2?

Adjusted R2 is the better model when you compare models that have a different amount of variables. The logic behind it is, that R2 always increases when the number of variables increases. Meaning that even if you add a useless variable to you model, your R2 will still increase.

Is higher R-squared better?

The most common interpretation of r-squared is how well the regression model fits the observed data. For example, an r-squared of 60% reveals that 60% of the data fit the regression model. Generally, a higher r-squared indicates a better fit for the model.

What is a good value of R-squared?

In other fields, the standards for a good R-Squared reading can be much higher, such as 0.9 or above. In finance, an R-Squared above 0.7 would generally be seen as showing a high level of correlation, whereas a measure below 0.4 would show a low correlation.

What is a good R value for correlation?

between -1 and 1

The relationship between two variables is generally considered strong when their r value is larger than 0.7. The correlation r measures the strength of the linear relationship between two quantitative variables. Pearson r: r is always a number between -1 and 1.