What are the accounting processes

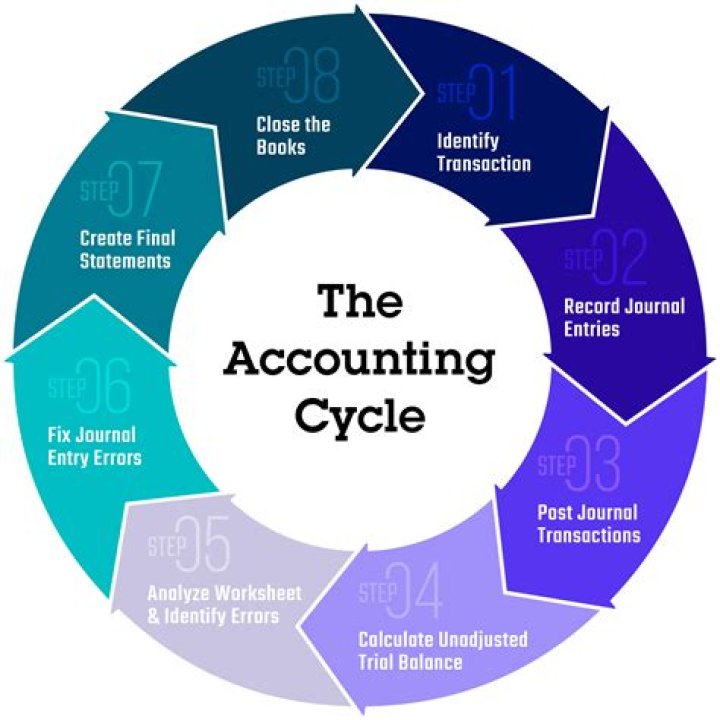

The eight steps of the accounting cycle are as follows: identifying transactions, recording transactions in a journal, posting, the unadjusted trial balance, the worksheet, adjusting journal entries, financial statements, and closing the books.

What are the 3 processes of accounting?

Part of this process includes the three stages of accounting: collection, processing and reporting.

What are the 5 steps in the accounting process?

Defining the accounting cycle with steps: (1) Financial transactions, (2)Journal entries, (3) Posting to the Ledger, (4) Trial Balance Period, and (5) Reporting Period with Financial Reporting and Auditing.

What are the four processes of accounting?

First Four Steps in the Accounting Cycle. The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance.What are the 6 steps in the accounting process?

- Journalizing Transactions.

- Posting to Ledger.

- Preparing Trial Balance.

- Making Adjusting Entries.

- Closing Temporary Entries.

- Compiling Financial Statements.

What are the 7 steps of accounting cycle?

We will examine the steps involved in the accounting cycle, which are: (1) identifying transactions, (2) recording transactions, (3) posting journal entries to the general ledger, (4) creating an unadjusted trial balance, (5) preparing adjusting entries, (6) creating an adjusted trial balance, (7) preparing financial …

What is accounting process or cycle?

The accounting cycle is a collective process of identifying, analyzing, and recording the accounting events of a company. It is a standard 8-step process that begins when a transaction occurs and ends with its inclusion in the financial statements.

What are the branches of accounting?

- Financial accounting. Financial accounting involves recording and clarifying business transactions along with preparation and presentation of financial statements. …

- Managerial accounting. …

- Cost accounting. …

- Auditing. …

- Tax accounting. …

- Fiduciary accounting. …

- Project accounting. …

- Forensic accounting.

What are the types of accounting?

- Financial accounting.

- Managerial accounting.

- Cost accounting.

- Auditing.

- Tax accounting.

- Accounting information systems.

- Forensic accounting.

- Public accounting.

The accounting cycle is a basic, eight-step process for completing a company’s bookkeeping tasks.

Article first time published onWhat are the 10 steps in the accounting cycle?

- Analyzing and Classify Data about an Economic Event.

- Journalizing the transaction.

- Posting from the Journals to General Ledger.

- Preparing the Unadjusted Trial Balance.

- Recording Adjusting Entries.

- Preparing the Adjusted Trial Balance.

- Preparing Financial Statements.

What are the steps of accounting cycle PDF?

- Identification of Transaction.

- Journalizing.

- Posting to Ledger.

- Preparation of Trial Balance.

- Adjusting Entry.

- Adjusted Trial Balance.

- Preparation of Financial Statement.

- Closing Entry.

What are the 11 steps in the accounting cycle?

- Analyze and measure financial transactions.

- Record transactions in Journal.

- Post information from Journal to General Ledger.

- Prepare unadjusted Trial Balance.

- Prepare adjusting entries.

- Prepare adjusted Trial Balance.

- Prepare financial statements.

- Prepare closing entries.

What are six steps in the accounting cycle quizlet?

- Analyze transactions.

- Journalize the transactions.

- Post the journal entries.

- Prepare a worksheet.

- Prepare financial statements.

- Record adjusting entries.

- Record closing entries.

- Prepare a postclosing trial balance.

Which is the last step of accounting process?

Answer: In the accounting cycle, the last step is to prepare a post-closing trial balance. It is prepared to test the equality of debits and credits after closing entries are made. Since temporary accounts are already closed at this point, the post-closing trial balance contains real accounts only.

What is basic accounting?

Basic accounting refers to the process of recording a company’s financial transactions. It involves analyzing, summarizing and reporting these transactions to regulators, oversight agencies and tax collection entities. … This is why businesses must be proficient in accounting in order to make good decisions.

What are the 12 steps of the accounting cycle?

- Prepare Journal Entries.

- Post the Journal Entries.

- Prepare the Unadjusted Trial Balance.

- Prepare Adjusting Journal Entries.

- Post the Adjusting Journal Entries.

- Prepare the Adjusted Trial Balance.

- Prepare the Income Statement.

- Prepare the Statement of Retained Earnings.

What are the 5 major transaction cycles?

- Revenue cycle—Interactions with customers. …

- Expenditure cycle—Interactions with suppliers. …

- Production cycle—Give labor and raw materials; get finished product.

- Human resources/payroll cycle—Give cash; get labor.

- Financing cycle—Give cash; get cash.

What are the 5 major types of accounting?

There are five main types of accounts in accounting, namely assets, liabilities, equity, revenue and expenses. Their role is to define how your company’s money is spent or received. Each category can be further broken down into several categories.

What are the 8 branches of accounting?

- Financial accounting.

- Cost accounting.

- Auditing.

- Managerial accounting.

- Accounting information systems.

- Tax accounting.

- Forensic accounting.

- Fiduciary accounting.

What are the 2 types of accounting?

The two main accounting methods are cash accounting and accrual accounting. Cash accounting records revenues and expenses when they are received and paid. Accrual accounting records revenues and expenses when they occur. Generally accepted accounting principles (GAAP) requires accrual accounting.

What are the 7 branches of accounting?

- Financial Accounting. Financial accounting is a systematic method of recording transactions of any business according to the accounting principles. …

- Cost Accounting. …

- Auditing. …

- Managerial Accounting. …

- Tax Accounting. …

- Forensic Accounting. …

- Fiduciary Accounting.

What are the six branches of accounting?

- Financial accounting.

- Management accounting.

- Cost accounting.

- Auditing.

- Taxation.

- Accounting Information Systems.

- Fiduciary Accounting.

- Forensic Accounting.

What are the 9 steps of accounting cycle?

- Identify all business transactions. …

- Record transactions. …

- Resolve anomalies. …

- Post to a general ledger. …

- Calculate your unadjusted trial balance. …

- Resolve miscalculations. …

- Consider extenuating circumstances. …

- Create a financial statement.

What are the main objectives of accounting?

The main objective of accounting is to keep a systematic record of financial transactions which helps the users to understand the day to day transactions in a systematic manner so as to gain knowledge about overall business.

What is the main product of accounting process?

We now come to the end-products or final outputs of the accounting process and the accounting cycle: the financial statements. There are five financial statements that are prepared, and will make up the financial reports of the company. Statement of Financial Position (Balance Sheet).

What are the 5 elements of financial statement?

To best understand financial statements, it’s important to understand the five elements of financial statements. Which are, assets, liabilities, equity, revenues and expenses.

What is workflow in accounting?

What is workflow? Workflow is an ‘organized and repeatable business activity enabled by the systematic organization of resources into processes.

What is 12th accounting cycle?

Accounting cycle is a process of recording all the financial transactions and processing them. When a complete sequence of recording and processing financial transactions is followed which happens frequently on a continuous basis during an accounting period is known as the accounting cycle.

What are the 8 steps in the accounting cycle quizlet?

- Step 1: Analyze Transactions. …

- Step 2: Journalize. …

- Step 3: Post. …

- Step 4: Prepare Worksheet. …

- Step 5: Prepare Financial Statements. …

- Step 6: Journalize Adjusting and closing entries. …

- Step 7: Post Adjusting and Closing Entries. …

- Step 8: Prepare Post-Closing Trial Balance.

What are the five characteristics that are common to all effective accounting systems?

- well planned.

- realistic.

- flexible.

- clearly communicated.

- evaluated.