What does the CAPM model tell us?

What does the CAPM model tell us?

The capital asset pricing model (CAPM) is an idealized portrayal of how financial markets price securities and thereby determine expected returns on capital investments. The model provides a methodology for quantifying risk and translating that risk into estimates of expected return on equity.

How do you use CAPM to value stock?

How is CAPM calculated? To calculate the value of a stock using CAPM, multiply the volatility, known as “beta,” by the additional compensation for incurring risk, known as the “Market Risk Premium,” then add the risk-free rate to that value.

How do you know if a stock is undervalued using CAPM?

CAPM, SML, and Valuations If a security’s expected return versus its beta is plotted above the security market line, it is considered undervalued, given the risk-return tradeoff.

How is CAPM used in real life?

Investors use CAPM when they want to assess the fair value of a stock. So when the level of risk changes, or other factors in the market make an investment riskier, they will use the formula to help re-determine pricing and forecasting for expected returns.

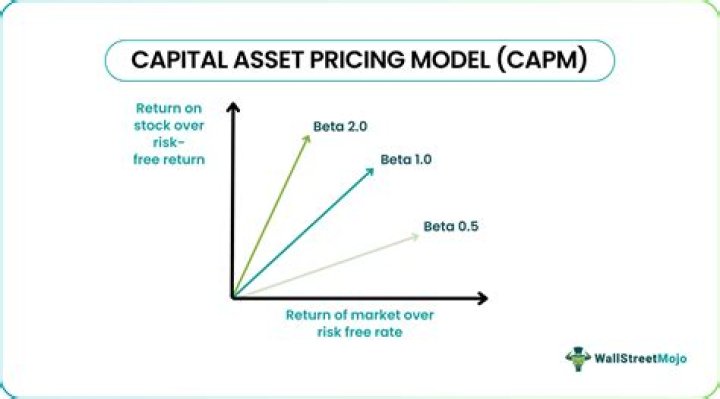

What is Beta in CAPM formula?

The beta (denoted as “Ba” in the CAPM formula) is a measure of a stock’s risk (volatility of returns) reflected by measuring the fluctuation of its price changes relative to the overall market. In other words, it is the stock’s sensitivity to market risk.

Why does the CAPM imply that investors should trade very rarely?

Why does the CAPM imply that investors should trade very rarely? Investors should trade very rarely because the market portfolio changes very rarely. (The market portfolio is a value-weighted portfolio and thus requires no additional trading when prices change to maintain the value weights).

How is CAPM calculated?

The capital asset pricing model provides a formula that calculates the expected return on a security based on its level of risk. The formula for the capital asset pricing model is the risk free rate plus beta times the difference of the return on the market and the risk free rate.

How is CAPM calculated example?

What is the expected return of the security using the CAPM formula? Let’s break down the answer using the formula from above in the article: Expected return = Risk Free Rate + [Beta x Market Return Premium] Expected return = 2.5% + [1.25 x 7.5%]

How do you know if a stock is overpriced or underpriced?

A stock is thought to be overvalued when its current price doesn’t line up with its P/E ratio or earnings forecast. If a stock’s price is 50 times earnings, for instance, it’s likely to be overvalued compared to one that’s trading for 10 times earnings.

What is the difference between SML and CML?

Difference between SML and CML CML is used to see a specific portfolio’s rate of return while the SML shows a market risk and a given time’s return. SML also shows the anticipated returns of individual assets. CML shows the total risk and measures it in terms of the SML (beta or systematic risk).

Why is CAPM wrong?

Research shows that the CAPM calculation is a misleading determination of potential rate of return, despite widespread use. The underlying assumptions of the CAPM are unrealistic in nature, and have little relation to the actual investing world.

Can CAPM be negative?

A negative interest rate makes no difference for CAPM, zero is just another number. Under negative interest rates, investors would hold lower volatility portfolios of risky assets than they would under positive interest rates.