What is the catch of refinancing?

What is the catch of refinancing?

The catch with refinancing comes in the form of “closing costs.” Closing costs are fees collected by mortgage lenders when you take out a loan, and they can be quite significant. Closing costs can run between 3–6 percent of the principal of your loan.

Is refinancing a waste of money?

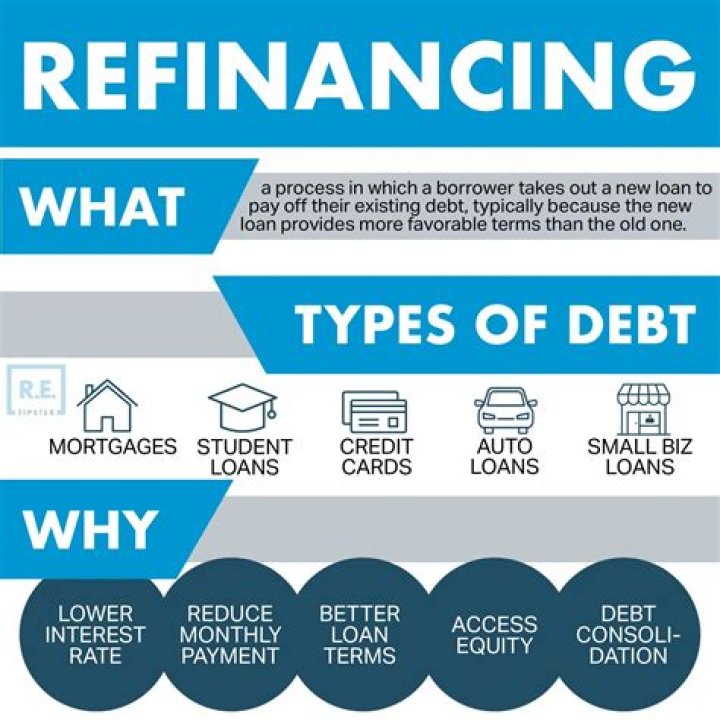

As a refresher, when you refinance your mortgage, you get a new loan that pays off your existing debt. Doing so can result in lower monthly payments unless you take out a substantial amount in cash. In general, you should avoid refinancing your mortgage if you’ll waste money and increase risk.

Is refinancing a good idea right now?

One of the best reasons to refinance is to lower the interest rate on your existing loan. Historically, the rule of thumb is that refinancing is a good idea if you can reduce your interest rate by at least 2%. However, many lenders say 1% savings is enough of an incentive to refinance.

What is the average closing cost on a refinance?

Mortgage refinance closing costs typically range from 2% to 6% of your loan amount, depending on your loan size. National average closing costs for a refinance are $5,749 including taxes and $3,339 without taxes, according to 2019 data from ClosingCorp, a real estate data and technology firm.

Do you lose your equity when you refinance?

Yes, you can lose equity when you refinance if you use part of your loan amount to pay closing costs. But you’ll regain the equity as you repay the loan amount and as the value of your home increases.

What percentage difference Should you refinance?

The traditional rule of thumb is that it makes financial sense to refinance if the new rate is 2 percent or more below your existing interest rate. The new rate on a refinance must provide enough savings in monthly mortgage payment to justify the cost of refinancing.

How many times is your credit pulled when refinancing?

While the number of credit checks for a mortgage can vary depending on the situation, most lenders will check your credit up to three times during the application process.