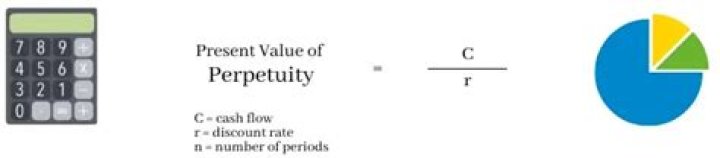

What is the perpetuity formula?

What is the perpetuity formula?

Perpetuity Present Value Formula It is the estimate of cash flows in year 10 of the company, multiplied by one plus the company’s long-term growth rate, and then divided by the difference between the cost of capital and the growth rate.

What is PVOA?

Present Value of an Ordinary Annuity (PVOA)

What is the formula for ordinary annuity?

Ordinary Annuity Formula refers to the formula that is used in order to calculate present value of the series of equal amount of payments that are made either at the beginning or end of period over specified length of time and as per the formula, present value of ordinary annuity is calculated by dividing the Periodic …

How much is an annuity worth?

An annuity will distribute a guaranteed income between $4,167 and $12,110 per month for a single lifetime and between $3,750 and $11,149 per month for a joint lifetime (you and spouse). Income amounts are factored by the age you purchase the annuity contract and the length of time before taking the income.

What is the formula for calculating annuity?

Annuity = r * PVA Ordinary / [1 – (1 + r)-n]

- PVA Ordinary = Present value of an ordinary annuity.

- r = Effective interest rate.

- n = Number of periods.

How do you use perpetuity formula?

Perpetuity Example First of all, we know that the coupon payment every year is $100 for an infinite amount of time. And the discount rate is 8%. Using the formula, we get PV of Perpetuity = D / r = $100 / 0.08 = $1250.

What is the present value of a 4 year ordinary annuity of $2 250?

Correct Answer: Option E. $10,446.

How annuity formula is derived?

Annuity derivation The formula for the present value of a regular stream of future payments (an annuity) is derived from a sum of the formula for future value of a single future payment, as below, where C is the payment amount and n the period.

How do you calculate an annuity?

To calculate using the annuity method of depreciation, you determine the internal rate of return (IRR) on the asset’s cash inflows and outflows, then multiply by the initial book value of the asset, then subtracted from the cash flow for the period of time that is being assessed.